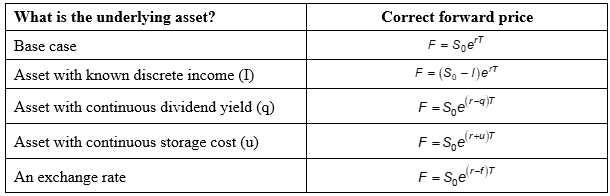

Financial Derivatives: Pricing and Arbitrage Opportunities

Closing Positions and Cash Settlement

To close a short or long position, enter a futures position of equal magnitude but opposite direction. If a position isn’t closed before contract expiry, the futures exchange calculates profit or loss and adjusts the account accordingly. For example, SPI200 futures contracts have a standard size of $A25.

Hedging Contracts

The number of contracts to hedge is calculated as: No of contracts = Beta * (value to be hedged / value of one SPI200)

Capital Asset Pricing Model (CAPM)

Return of portfolio = risk-free rate + beta * (market return – risk-free rate)

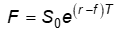

Forward Price with Two Exchange Rates

r = local rate and f = foreign rate

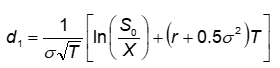

Black-Scholes Formula for Call Option Value

Where N(.) represents a standard normal cumulative distribution function, found on Z table or using NORM.S.DIST in Excel.

Put-Call Parity

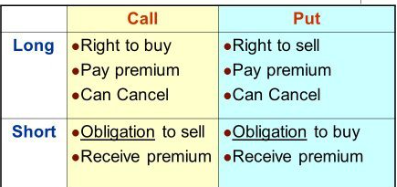

American vs. European Options

Arbitrage Opportunity for Long Call Option

Steps:

- Calculate the lower bound.

- If the option price is too low (less than the lower bound):

- Enter a long call position at the option price.

- Short sell shares at the current stock price.

- Invest the difference (short sale – option price) at the risk-free rate.

- If S < X, we exercise the call and gain the difference.

- If S > X, we exercise the call, pay the spot price to close the short position, and receive the invested surplus.

- Profit in both scenarios.

- Example: An American-style call option on Suncorp with three months to expiry, a strike price of $4.50, trading at $1.20. Suncorp shares are at $6.00, with a 5% risk-free interest rate.

Immediate exercise yields a $0.30 profit (buy at $4.50, sell at $6, less option price $1.20).

Arbitrage Opportunity for Long Put Option

Steps:

- Calculate the lower bound.

- If the option price is lower than the lower bound:

- Enter a long put option.

- Buy shares at the current spot price.

- Exercise the right to sell at the strike price.

- Profit = (strike price – spot price) + option price.

- Example: Strike price $7.50, spot price $6.90, option price $0.35, profit = $0.25.

Arbitrage Opportunity for Short Call Option

Steps:

- Calculate the upper bound (stock price).

- If the option premium is higher than the stock price:

- Short call and receive the premium.

- Buy stock.

- Invest the difference.

- If S < 10, the option expires worthless.

- If S > 0, the option is exercised. Losses are recouped by selling stock.

- Example: Call option on XYZ with a $10 strike, current price $8.50, premium $9.

Arbitrage Opportunity for Short Put Option

Steps:

- Calculate the upper bound (strike price).

- If the option premium is higher than the strike price:

- Short put and receive the premium.

- Invest everything in the bank.

- If S > strike price, the option is not exercised.

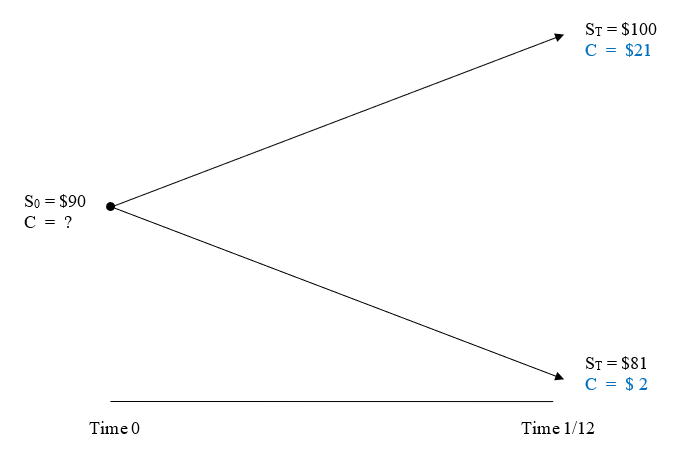

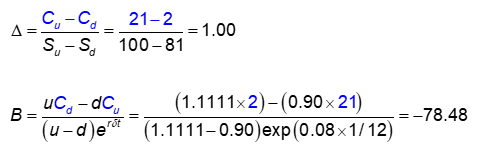

Binomial Tree

S0 is the current strike price at time 0. St (Su) = $100 if price goes up, St (Sd) = $81 if prices go down. C = call option payoff.

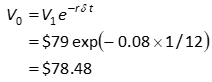

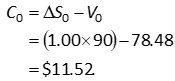

Replication Approach

Construct a portfolio of ∆ shares and borrowed money to match the option payoff. Example:

Purchase 1 share and borrow $78.48. Construction cost = (∆ * S) – B = (1 * 90) – 78.48 = 11.52.

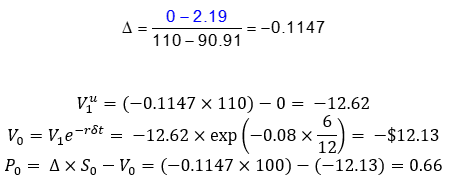

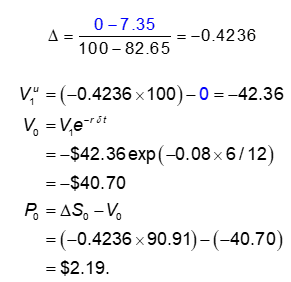

Delta Hedging Method

Create a portfolio with ∆ stocks and a short option for a certain payoff. Discount to present value to find the option price. Example:

V1 is the payoff. Vu and Vd should be equal. Delta hedging can also be used with put options.

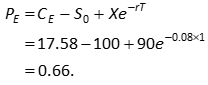

Payoff can also be found using the Black-Scholes formula.

Calculate Up Movement

Calculate Down Movement

d = 1/u

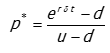

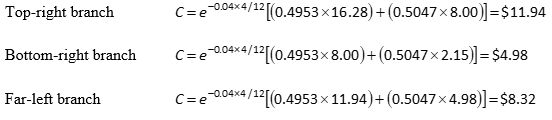

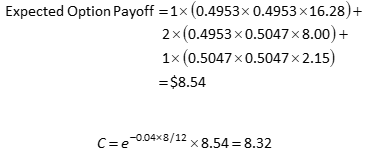

Risk-Neutral Valuation Method

Find P, the probability of up/down movements if individuals were risk-neutral.

1-P is the downward probability. Calculate the expected option payoff and discount back at the risk-free rate.

Example:

For European options, calculate all possible payoffs and path probabilities, then discount to time 0.

For American options, use the risk-neutral valuation method recursively.

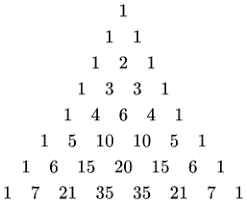

Pascal’s Triangle

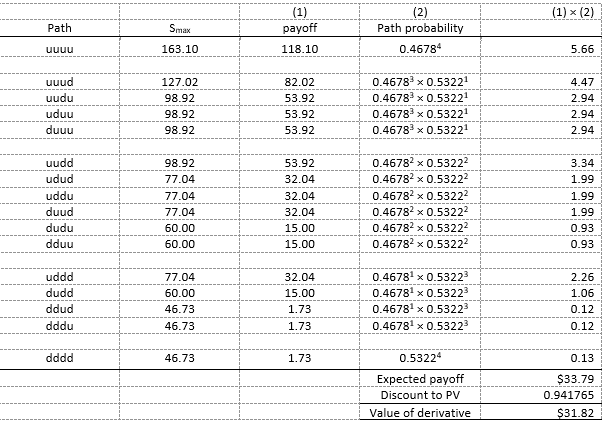

Path Dependent Payoff – Lookback Options

Floating lookback call: payoff = max(0, ST – Smin)

Floating lookback put: payoff = max(0, Smax – ST)

Fixed lookback call: payoff = max(0, Smax – X)

Fixed lookback put: payoff = max(0, X – Smin)

Steps:

- List all possible paths and find the max/min price.

- Calculate path probability and multiply by the payoff.

- Sum all potential payoffs.

- Discount to present value.

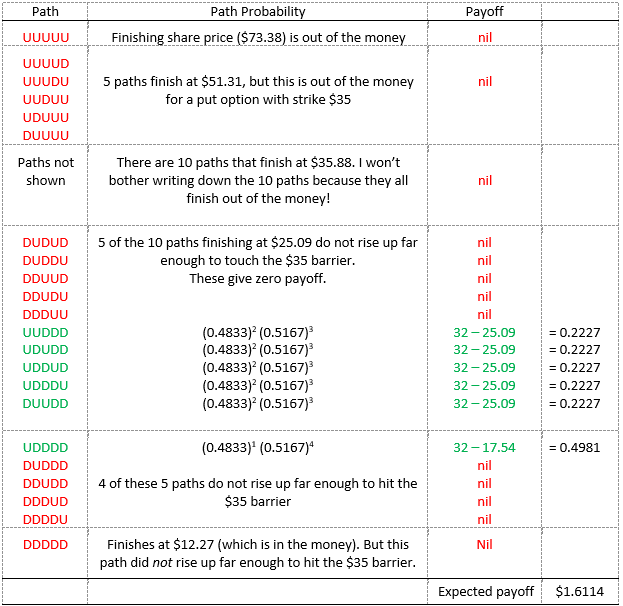

Path Dependent Payoff: Barrier Options

Like a normal binomial distribution, but we exclude all paths that are both not in the money and dont hit the barrier:

Exclude all nodes, and the paths to these nodes, which are out of the money

Exclude all nodes that are in the money, but do not hit the barrier during their path

Only use paths that are in the money and hit the barrier during their path

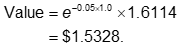

Find these payoffs as normal, multiplying the path probabilities by the payoff at the end, summing all these payoffs then discounting to present value

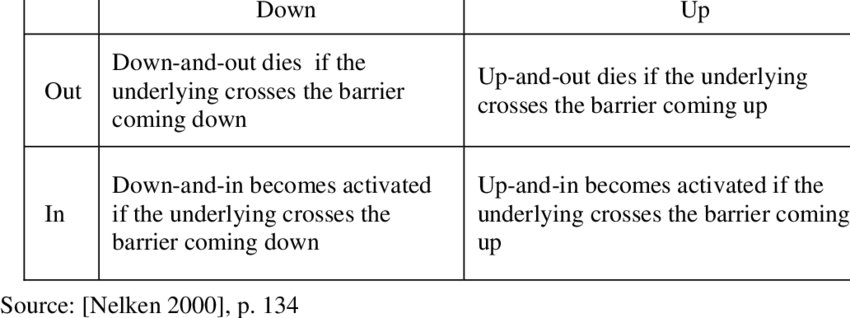

Remember the different types of barriers:

Up and in example ^

= Up if barrier (H) is above starting share price, = Down if H is below starting share price