Futures and Forwards: Hedging and Pricing Strategies

Chapter 2: Futures and Forwards

Futures Contract: A standardized contract traded on an exchange to buy or sell an asset at a future date at a price specified today. It can lead to losses if the price of the underlying asset goes up in the future.

Forward Contract: A customized contract between two parties to buy or sell an asset at a future date for a price agreed upon today. It can lead to profits if the price of the underlying asset goes up in the future.

Cash Flows: In a forward contract, no cash is exchanged upfront; profits/losses occur only at maturity. In futures contracts, gains/losses are settled daily via the marking-to-market process.

Marking-to-market: Adjusting the value of a futures contract daily to reflect changes in market prices.

Mechanics of Futures and Forward Contracts & Markets

Futures markets: Exchange-based, standardized contracts, typically requiring margin.

Forward markets: Over-the-counter (OTC), non-standardized contracts, with higher counterparty risk. Margin requirements in futures contracts reduce credit risk by requiring collateral.

Difference between Forward and Futures Markets

Liquidity: Futures markets are more liquid due to standardization.

Counterparty Risk: Higher in forward contracts since they are not cleared through a centralized exchange.

Convergence of Spot and Futures Price: As the contract approaches maturity, the futures price tends to converge to the spot price of the underlying asset due to arbitrage opportunities.

Profits at maturity

Profit to Long (Buyer): Spot price at maturity (ST) – Original Futures Price

Profit to Short (Seller): Original Futures Price (F0) – Spot price at maturity (ST)

What if Spot and Futures Price of gold are not equal close to contract maturity?

Suppose P(futures) = $30/oz and P(spot) = $29.50/oz on the last trade day of the contract. To make a profit one can:

- Sell futures contract (enter short position).

- Buy gold on the spot market @ 29.50/oz

- Make a delivery of gold to long position holder and get @ $30/oz

- Profit $30 – $29.5 = $0.50 /oz

Chapter 3: Hedging using futures

Purpose of Hedging

Hedging is used to manage price risk and reduce exposure to volatility in the underlying asset.

Setting Up a Long and Short Hedge

Long Hedge: Used when you expect to buy the asset in the future and want to lock in a price. Example: A company expecting to purchase raw materials in the future may go long on futures.

Short Hedge: Used when you plan to sell the asset in the future and want to lock in a selling price. Example: A farmer expecting to sell crops may go short on futures.

Basis Risk

Basis = Spot Price – Futures Price

Basis Risk: The risk that the futures price and the spot price will not move perfectly in sync, leading to imperfect hedging outcomes

In the spot market for oil, the distributor always realizes the spot price ST in February by selling to the client. In the futures markets, the distributor has a short position and realizes F1 – ST in February, by entering an offsetting long position on the maturity date (remember FT = ST by convergence property). The effective price realized is therefore ST + (F1 – ST) = F1= $97.15 per barrel. Assume that the oil distributor’s acquisition/production cost per barrel is $90. Distributor’s profit = $97.15 – $90 = $7.15 per barrel or $750,000 in total, no matter what happens to the spot price

Choice of Contract

The ideal futures contract for hedging should have the closest expiration date to the period of exposure and involve the same or closely related underlying asset.

Rolling Hedge Forward

If the exposure period exceeds the maturity of the futures contract, a position can be “rolled forward” by closing out the current position and entering into a new one with a later expiration date.

Arguments For and Against Hedging

For Hedging:

Reduces the risk of adverse price movements and ensures stable costs/revenues.

Against Hedging:

Hedging costs (commissions, bid-ask spreads) and the opportunity cost of locking in prices.

How and When to Hedge

Hedge when you have significant exposure to price volatility in the future. The type of hedge (long or short) depends on your future position in the asset.

F1: Initial Futures Price, at which contract is initiated

F2: Final Futures Price, when contract is closed out

S2: Final Asset Price, at the time when contract is closed out

You hedge the future sale of an asset by entering into a short futures contract

Chapter 5: Pricing Futures and Forwards

Review Continuous and Discrete Interest

Continuous Interest: e^(rt) where r is the interest rate and t is time.

Discrete Interest: (1+r)^t Use these formulas to calculate present and future values of cash flows.

Price Realized=S2+ (F1 – F2) = F1 +(S2 – F2) = F1 + Basis

S2 – price realized in the spot market, (F1 – F2) profit on short futures position. In the Oil distributor example, S2 and F2 were uncertain February Spot and Futures prices, respectively, and F1 = $97.15 per barrel. Price realized = S2+ ($97.15 – F2) = 97.15 + (S2 -F2), but because the contract expiration month matches exactly the expiration of the hedge (February 2021), S2 = F2 or zero basis. Oil distributor locked in 97.15

Futures-Spot Parity (No Arbitrage Arguments)

No Arbitrage: The relationship between the futures price and the spot price must prevent arbitrage opportunities.

Cases to Consider

Investment Asset with Known Income: Adjust futures price for income expected from the asset during the life of the contract.

Investment Asset with Known Yield: Similar to known income, but adjusted for percentage yield.

Futures-Spot Parity in Foreign Exchange Markets: Futures price reflects the interest rate differential between two currencies.

Storage Cost: When the underlying asset has storage costs, the futures price includes these costs.

Pricing Futures of Consumption Assets

Future Spot Parity for Consumption Assets: Prices reflect supply/demand and consumption value (i.e., the convenience yield).

Futures-Spot Parity: F=S(1+r)^t | Basis = S – F | Cost of Carry: F= Se^((r+c-y)*t) | c: cost of carry (storage cost) | y: convenience yield

Cost of Carry and Convenience Yield

Cost of Carry: The cost of holding an asset until the delivery date (storage, insurance, etc.).

Convenience Yield: The non-monetary benefit of holding a physical asset rather than a futures contract.

Term Structure of Forward Rates

Forward rates across different maturities form a term structure that reflects expectations about future spot rates.

S0: Spot price today

F0: Futures or forward price today

T: Time until delivery date

r: Risk-free interest rate for maturity T

Future Value When Interest is Compounded Once a Year

FV = PV ·(1+r)T

This equation relates the Future Value (FV) and Present Value (PV) when interest is compounded once a year. Example: PV = $1000, r = 5% per annum (p.a.) compounded once a year, T = 2 years FV = 1000∙(1+0.05)2=1102.50

Future Value When Interest is Compounded more than Once a Year

FV = PV ·(1+r/m)^(T·m)

This equation relates the Future Value (FV) and Present Value (PV) when interest is compounded more than once a year. Example: PV = $1000, r = 5% p.a. compounded quarterly (m=4), T = 2 years, FV = 1000∙(1+0.05/4)^(2∙4)=1104.49

Future Value When Interest is Continuously Compounded

FV = PV ·e^(rT)

This equation relates the Future Value (FV) and Present Value (PV) when interest is compounded continuously. Note that e = 2.71828, it is the base of natural logarithms. Example: PV = $1000, r = 5% p.a. compounded continuously, T = 2 years, FV = 1000∙e0.05∙2=1105.17 Compare it to the case with once-a-year compounding: FV = 1000∙(1+0.05)2=1102.50 All else equal, more frequent compounding increases FV.

Present Value when Interest is Continuously Compounded

PV = FV· e^(-rT)

Example: FV = 1105.17, r = 5% p.a. compounded continuously, T = 2 PV = 1105.17 *e^(-0.05·2)= 1000

How interest rates relate

Rc = m * ln(1+ Rm/m) | Rc= interest rate with continuous compounding, Rm = interest rate compounded m times a year, ln = natural log function

Consider an interest rate quoted as 10% per annum with semiannual compounding; m = 2 and Rm = 0.1, the equivalent rate with continuous compounding is 2ln(1+0.½) = 0.09758 or 9.758% per annum.

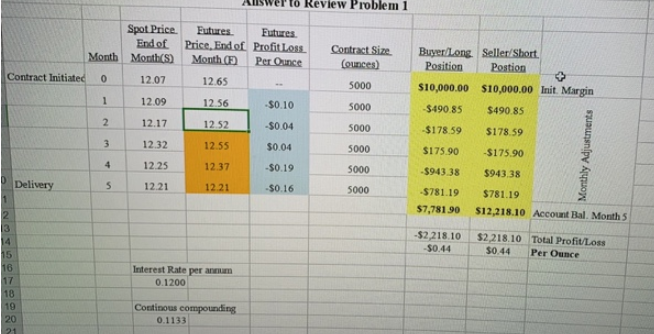

Problem 1

Consider the Mark-to-Market Settlements for 1 silver futures contract maturing in 5 months. Assume that the risk-free rate available to investors is 12% per annum with annual compounding and that Futures-Spot parity with continuous compounding holds in all months. Also assume that the initial margin is $10,000, while the maintenance margin is $7000.

a. In the table above, show your answers in the cells marked by “a”

First convert 12% per annum with annual compounding into a rate based on continuous compounding. Rc = m * Ln(1+Rm/m) = 1 * Ln(1+0.120/1) = 0.1133 or 11.33%. The result makes sense, as it takes a lower rate to yield the same future value with more frequent compounding.

Problem 2

You work as a trader for the arbitrage desk at Goldman Sachs, monitoring spot and futures foreign exchange rates. At 10 am Eastern time you observe the following market prices and rates. The spot exchange rate between US$ and Canadian dollar is $1.0500/C$, while the futures price of the Canadian dollar for the contract maturing in 3 months is $1.1500/C$. The US 3-month interest rate is 8% per annum, while the Canadian 3-month interest rate is 4% per annum. Both interest rates are based on continuous compounding.

(a) What is the no-arbitrage exchange rate?

Consider information known today: So = $1.0500/C$, Fo = $1.1500/C$, r = 0.08 and rf = 0.04

No-arbitrage exchange rate or Futures-Spot parity exchange rate is

Fo (no-arbitrage) = 1.0500 * e^((0.08 – 0.04)*0.25) = $1.0605/C$. Recall, e = 2.71828

(b) Given your answer in part (a) and data provided, describe the arbitrage strategy that will earn profit and calculate your profit, assuming that you can lend or borrow 1000 units of a currency. Note that Fo > Fo (no arbitrage), suggesting that you can sell relatively expensive Canadian dollars on the forward market, and buy relatively cheap Canadian dollars on the spot market.

- Today borrow $1,000 at 8% per annum for 3 months, convert to 1,000/1.05 = 952.38 C$ and invest Canadian dollars at 4% for 3 months. Note that:

- In 3 months you will have to repay $1000e^(rT) = 1000 e^*(0.08*0.25) = $1020.20, and

- Also in 3 months you will earn 952.38 e^(rf*T) = 952.38 e^(0.04*0.25) = 961.95 C$

- Today enter a forward contract to sell 961.95 C$ for 961.95C$*1.1500 = $1106.24

- In 3 months you will:

- Collect on your investment 961.95 C$

- Deliver these 961.95 C$ to satisfy your short forward contract obligation and get $1106.24 in exchange (remember Fo = $1.1500/C$).

- Repay principal and interest on your loan in the amount of $1020.20

Your profit = $1106.24 – $1020.20 = $86.04

Problem 3.

It’s September 2010. You are an oil distributor, planning to sell 100,000 barrels of crude oil to a client in February 2011 in exchange for a spot price prevailing at that time. Because the February 2011 spot price is unknown today, your objective is to hedge this risk. The futures price of crude oil for February 2011 delivery is $97.15. The contract size for crude oil is 1000 barrels. Assume that there is no excessive volatility during the delivery month.

(a) If you were to hedge using the futures market, would you enter a short or long futures position?

Explain. A short position. To secure its revenues, the oil distributor would benefit from short hedging. If the spot price declines, the short futures position would gain and vice versa.

(b) What contracts and how many contracts do you need?

You would need to short 100 crude oil futures contracts maturing February 2011, at a futures price of $97.15 per barrel

(c) Calculate total profit or loss on your futures position, if at the futures contract’s maturity in February 2011 the spot price turns out to be $80.00 a barrel.

Profit = ($97.15 – $80.00) * 100 contracts * 1000 barrels per contract = $1,750,000. Note that at February 2011’s contract maturity, both the spot and contract’s futures price will be equal to $80 per barrel.

(d) Assume that the crude oil’s spot price in February 2011 turns out to be $80 per barrel. What is the overall price per barrel realized by the oil distributor in February 2011 after taking into account hedging profits or losses?

Price realized per barrel = Spot (in Feb. 2011) + ($97.15 – $80.00) = $80.00 + ($97.15 –$80.00) = $97.15

Investment Asset – Silver: An arbitrage opportunity

Case 1: Spot price of silver: 40/oz | Quoted 3-month forward price of silver: 43/oz | 1-year interest rate is 5% per annum | No income or storage costs for silver

Case 1: Now: Borrow 40 at 5% for 3 months. Buy one unit of asset. Enter into a forward contract to sell the asset in 3 months for $43. Action in 3 months: Sell the asset for $43. Use $40.50 to repay the loan with interest. Profit realized $2.50 | Buy spot, Short forward position

Case 1: Today the forward price for a 3-month contract is Fo = $43/oz, and the amount borrowed is $40. In 3-months, the investor has to repay 40 *e^((0.05∙(3/12)) | . Profit = Fo – So*e^(r*T) = 43 – 40 ∙e^(0.05∙3/12) = $2.50 l This profit is risk-free, today’s stock price, forward price, and the amount of loan to be repaid are known today.

Case 2: Spot price of silver: 40/oz | Quoted 3-month forward price of silver: 39/oz | 1-year interest rate is 5% per annum | No income or storage costs for silver

Case 2: Now: Short 1 unit of asset to realize $40. Invest $40 at 5% for 3 months. Enter into a forward contract to buy the asset in 3 months for $39. Action in 3 months: Buy Asset for $39. Close short position. Receive $40.50 from investment. Profit Realized: $1.50 | Case 2: Sell short Spot, Long forward position

Case 2: Today the forward price for a 3-month contract is Fo = $39/oz, and the amount invested is $40. In 3-months, the investor will obtain 40 ∙e^(0.05∙3/12) | Profit = So*e^(r∙T) – Fo = 40 ∙e^(0.05∙3/12) – 39 = $1.50 | This profit is also risk-free, today’s stock price, forward price, and the amount to be received from the investment are known today.

Action by many investors in pursuit of the risk-free profit will put pressure on both spot and forward prices today. | If Fo = $43 and So = $40, investors will keep buying silver on the spot market, bidding up its spot price and short silver forwards lowering its forward price. | If Fo = $39 and So = $40, investors will keep short selling silver on the spot market, pushing its spot price down and keep entering long silver forwards increasing its forward price. | Such arbitrage action will cease when risk-free profit is no longer available. That is when Profit = 0. This happens when Fo = So∙e^(r∙T). This equation relates the forward price and the spot price for any investment asset that provides no income and has no storage costs. Also, the formula applies only when interest rates are measured with continuous compounding

When an Investment Asset Provides a Known Yield

F0 = S0 *e^((r–q)∙T) where q is the average yield during the life of the contract (expressed with continuous compounding). A bond priced at $900 has an annual coupon yield of 10%. With continuous compounding, this yield translates to 1*ln(1+0.10)=0.0953 or 9.53% per annum. With a risk-free rate with continuous compounding set at 10% p.a., a forward contract on a stock maturing in 2 years priced at time 0 at F0 = 900 ·e^((0.10–0.0953)∙2)=908.50

Futures and Forwards on Currencies: A foreign currency is analogous to a security providing a dividend yield. The continuous dividend yield is the foreign risk-free interest rate l It follows that if rf is the foreign risk-free interest rate, r is the domestic risk-free rate, So is the spot exchange rate, and Fo is the forward exchange rate, then: F0=S0*e^((r-rf)* T)

When F0 > S0*e^((r-rf)* T) an arbitrageur buys foreign currency spot and sells foreign currency futures/forwards

When F0

Futures on Investment Commodities: No Arbitrage Pricing Principle

New factor – storage cost must be incurred to conduct arbitrage F0 = S0 e^((r+u)T)

where u is the storage cost per unit time as a percent of the asset value.

Alternatively, F0 = (S0+U)e^(rT) where U is the present value of the storage costs.