Key Accounting Principles and Financial Ratios

Accounting information helps users evaluate the amount, timing, and uncertainty.

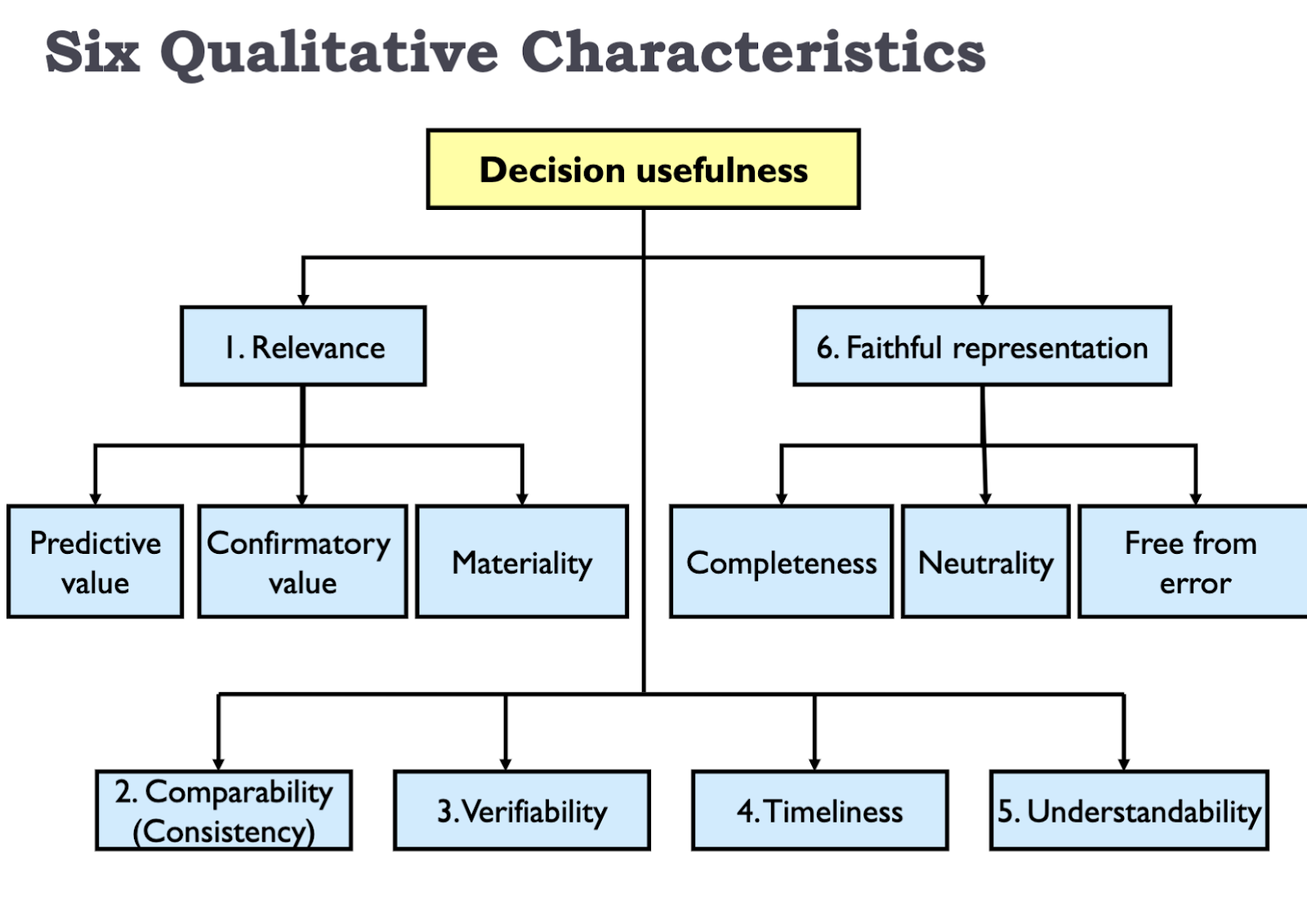

Key Accounting Principles

- Relevance: Pertinent to the decision at hand.

- Predictive Value: Information is useful in predicting the future.

- Confirmatory Value: Information confirms expectations.

- Materiality: Concerns the relative size of an item and its effect on decisions.

- Faithful Representation: Agreement between the measure and the phenomenon it purports to represent.

- Completeness: Includes all information necessary for faithful representation.

- Neutrality: Implies that financial accounting standards are free from bias.

- Free from Error: Information has no errors or omissions (not excluding anything).

- Comparability: Important for making inter-firm comparisons.

- Consistency: Applying the same accounting practices over time.

- Verifiability: Implies consensus among different measures.

- Timeliness: Information is available prior to the decision.

- Understandability: Users understand information in the context of the decision being made.

- Cost Effectiveness: Benefits exceed costs of sharing information with external users.

Key Accounting Concepts

- Recognition: Process of admitting information into statements.

- Comprehensive Income: Change in equity from non-owner transactions.

- Distribution to Owners: Decrease in equity resulting from transfers to owners.

- Earnings Quality: Ability of reported earnings to predict a company’s future earnings.

- Permanent Earnings: Anticipated/expected income over a long time period.

- Transitory Earnings: Unexpected income fluctuations (e.g., lottery).

- Discontinued Operations: Operating segment that either has been disposed of or is classified as held for sale and represents a major business line or geographical area of operations.

Key Financial Ratios

- Basic EPS: (Net Income – Preferred Dividends) / Weighted Average Number of Common Shares Outstanding for Period

- Diluted EPS: (Net Income – Preferred Dividends) / (Weighted Average Number of Common Shares Outstanding for Period + Diluted Securities)

- Net Profit Margin: Net Income / Revenue

- Gross Profit Margin: Gross Profit / Revenue

- Operating Profit Margin: Operating Profit / Revenue

- Pretax Profit Margin: Pretax Profit / Revenue

- Cash Ratio: (Cash + Marketable Securities) / Current Liabilities

- Quick/Acid Test: (Cash + Marketable Securities + Receivables) / Current Liabilities

- Current Ratio: Current Assets / Current Liabilities

- ROE: Net Income/ Average Equity = Net Income / Average Assets x Average Assets / Average Equity = ROA x Leverage

- ROA: Net Income / Average Assets = Net Income / Revenue x Revenue / Average Assets

- Inventory Turnover: COGS/ Average Inventory

- Receivables Turnover: Revenue/ Average Receivables

- Payables Turnover: (COGS + Net Change in Inventory) / Average Trades Payables

- Days of X: 365/ X Ratio

- Cash Conversion/Net Operating Cycle: Days Receivables + Days Inventory Held – Days of Payables

Four Approaches to Expense Recognition

- Based on exact cause and effect relationships (e.g., COGS).

- Associating an expense with revenues recognized in a specific time period (e.g., salaries).

- By a systematic and rational allocation to specific time periods (e.g., depreciation and amortization).

- In the period incurred, without regard to related expenses (e.g., advertising).

Five Types of Measurement

- Historical Costs: Original transaction value.

- Net Realizable Value: Estimated amount of cash into which the asset/liability will be converted (e.g., A/R).

- Current Cost: Cost that would be incurred to purchase or reproduce the asset (e.g., inventories are valued at lower of cost or market).

- Present Value: Discounted future cash flows (e.g., bonds).

- Fair Value: Current market value (e.g., trading securities).

*If market value is not available, use a) value of similar assets or b) derived value based on pricing models.

GAAP vs. IFRS

-GAAP hierarchy is Congress, SEC, private sector (CAP, APB, now FASB).