Understanding Financial Accounting: Assets, Liabilities, and Equity

Return on Assets: A Key Profitability Metric

A crucial measure of profitability is the return on assets (ROA). It helps stakeholders determine if a company is using its assets effectively. Asset turnover indicates how efficiently a company utilizes its assets to generate sales—specifically, how many dollars of sales are generated for each dollar invested in assets. Profit margin reveals how effectively a company converts sales into income.

To increase its return on assets, a company can:

- Increase the margin it generates from each dollar of goods sold (profit margin).

- Increase the volume of goods sold (asset turnover).

Accounting for Assets

Companies record as debits (increases) to the Land account all necessary costs incurred to make land ready for its intended use.

Companies debit to the Buildings account all necessary expenditures related to the purchase or construction of a building.

Obsolescence is the process by which an asset becomes outdated before it physically wears out.

Repairs are debited to Maintenance and Repairs Expense as they are incurred. Because they are immediately charged as an expense against revenues, these costs are often referred to as revenue expenditures.

Additions and improvements are costs incurred to increase the operating efficiency, productive capacity, or useful life of a plant asset. They occur infrequently and are often referred to as capital expenditures. These amounts are debited to the plant asset affected.

Leasing Assets

A lease offers several advantages:

- Reduced risk of obsolescence.

- Little or no down payment.

- Shared tax advantages.

Depreciation of Plant Assets

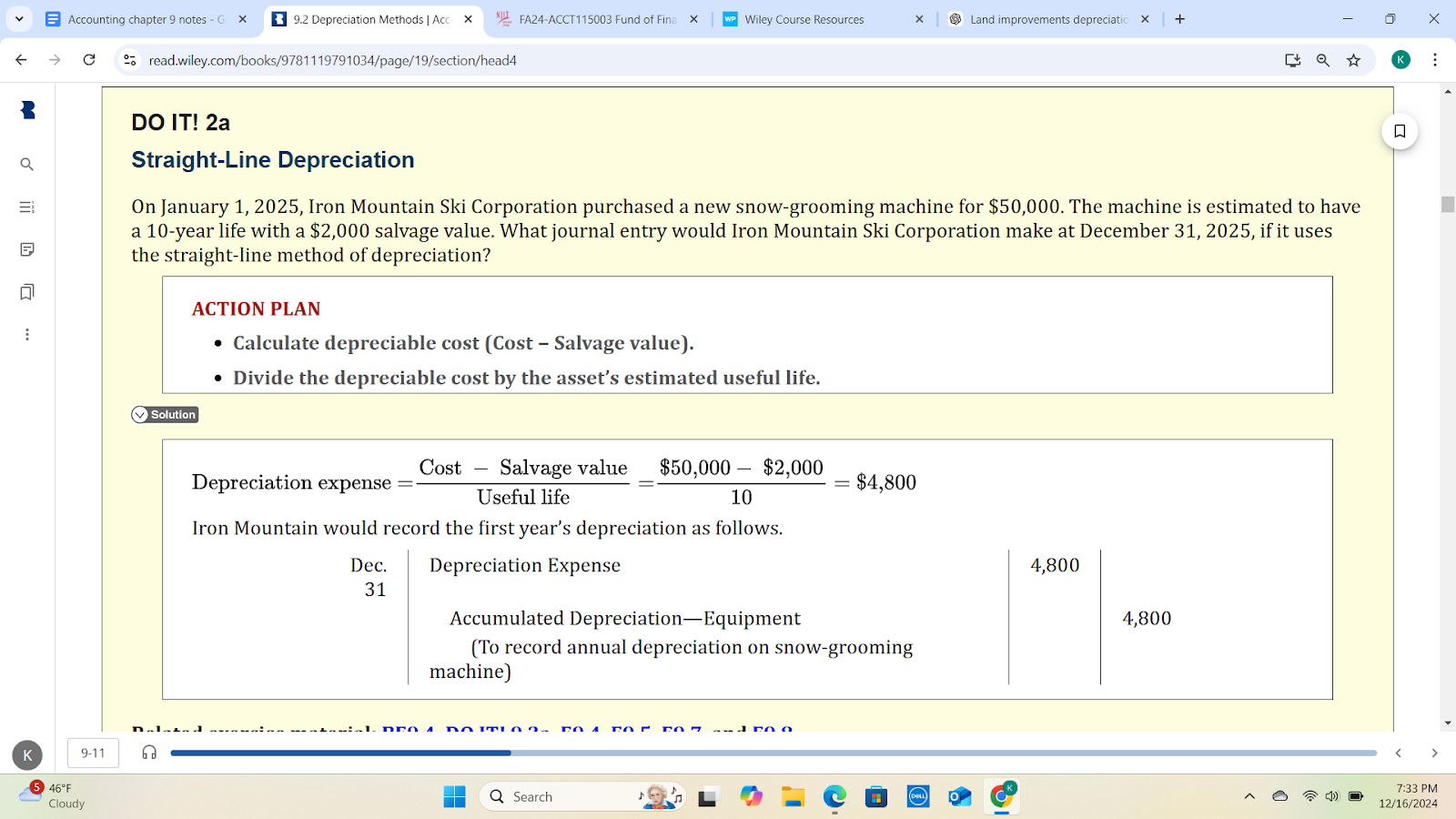

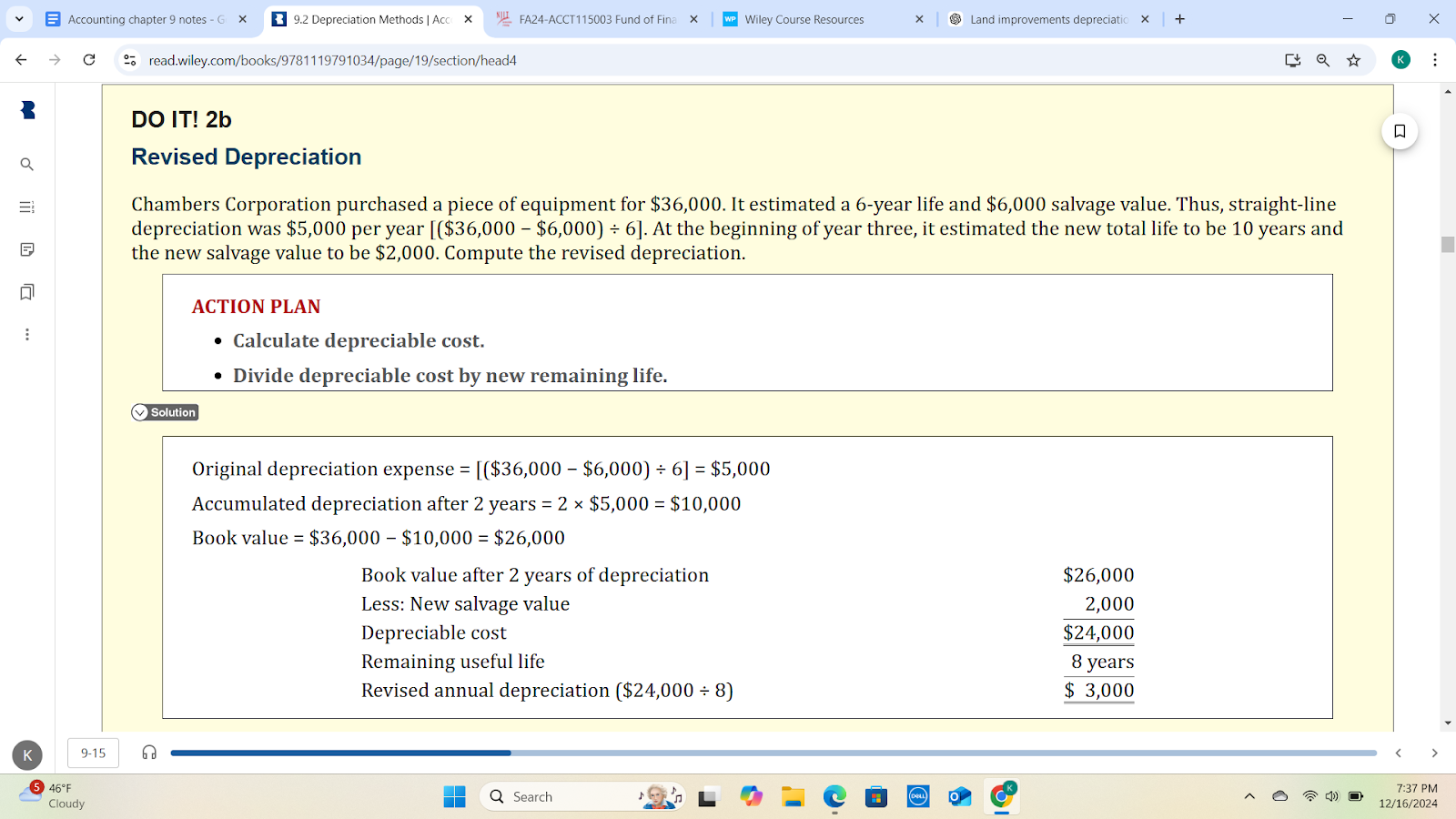

Depreciation is the process of allocating the cost of a plant asset over its useful (service) life in a rational and systematic manner. It applies to three classes of plant assets: land improvements, buildings, and equipment (excluding land).

A permanent decline in the fair value of an asset is referred to as an impairment. This is recorded by debiting a loss and crediting accumulated depreciation.

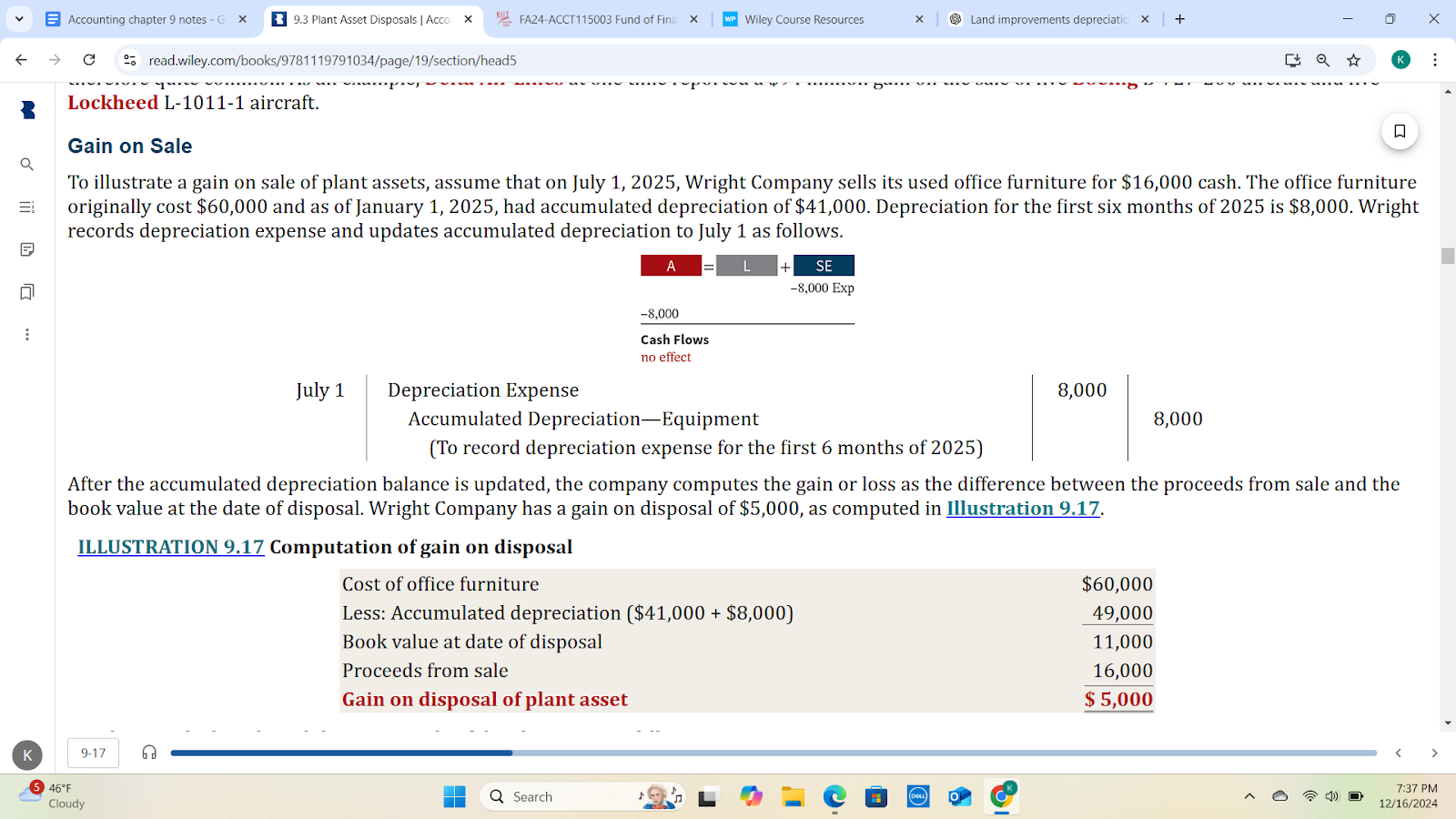

Disposal of Plant Assets

When disposing of an asset, the company removes the asset’s book value by debiting (reducing) the Accumulated Depreciation account for the total depreciation up to that point.

The company also credits (reduces) the Asset account to remove the original cost of the asset from the books.

Retirement of Plant Assets

Companies decrease (debit) Accumulated Depreciation for the full amount of depreciation taken over the asset’s life and decrease (credit) the asset account for the original cost of the asset.

Accounting for Intangible Assets

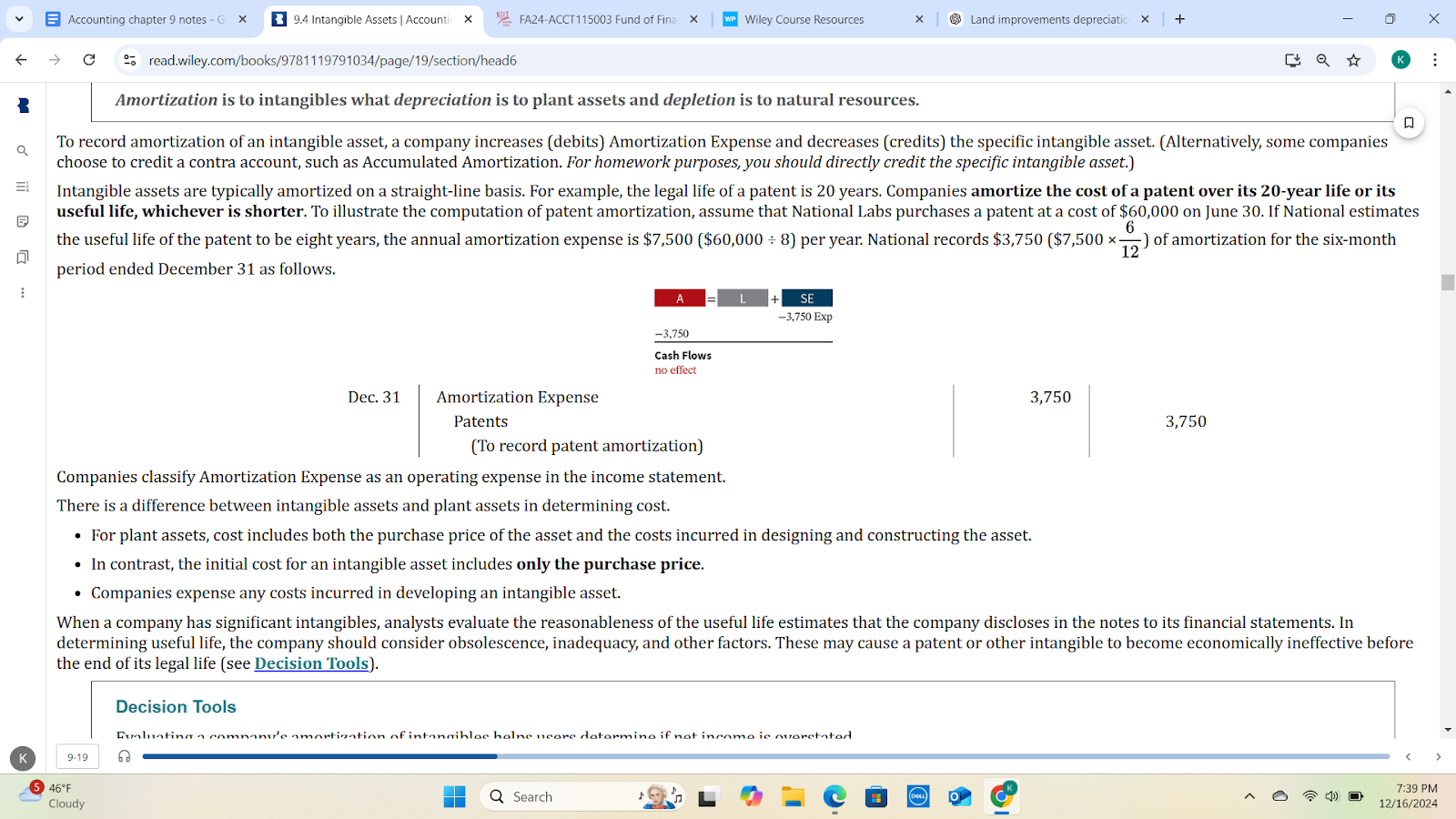

The process of allocating the cost of intangibles is referred to as amortization. To record amortization, a company increases (debits) Amortization Expense and decreases (credits) the specific intangible asset.

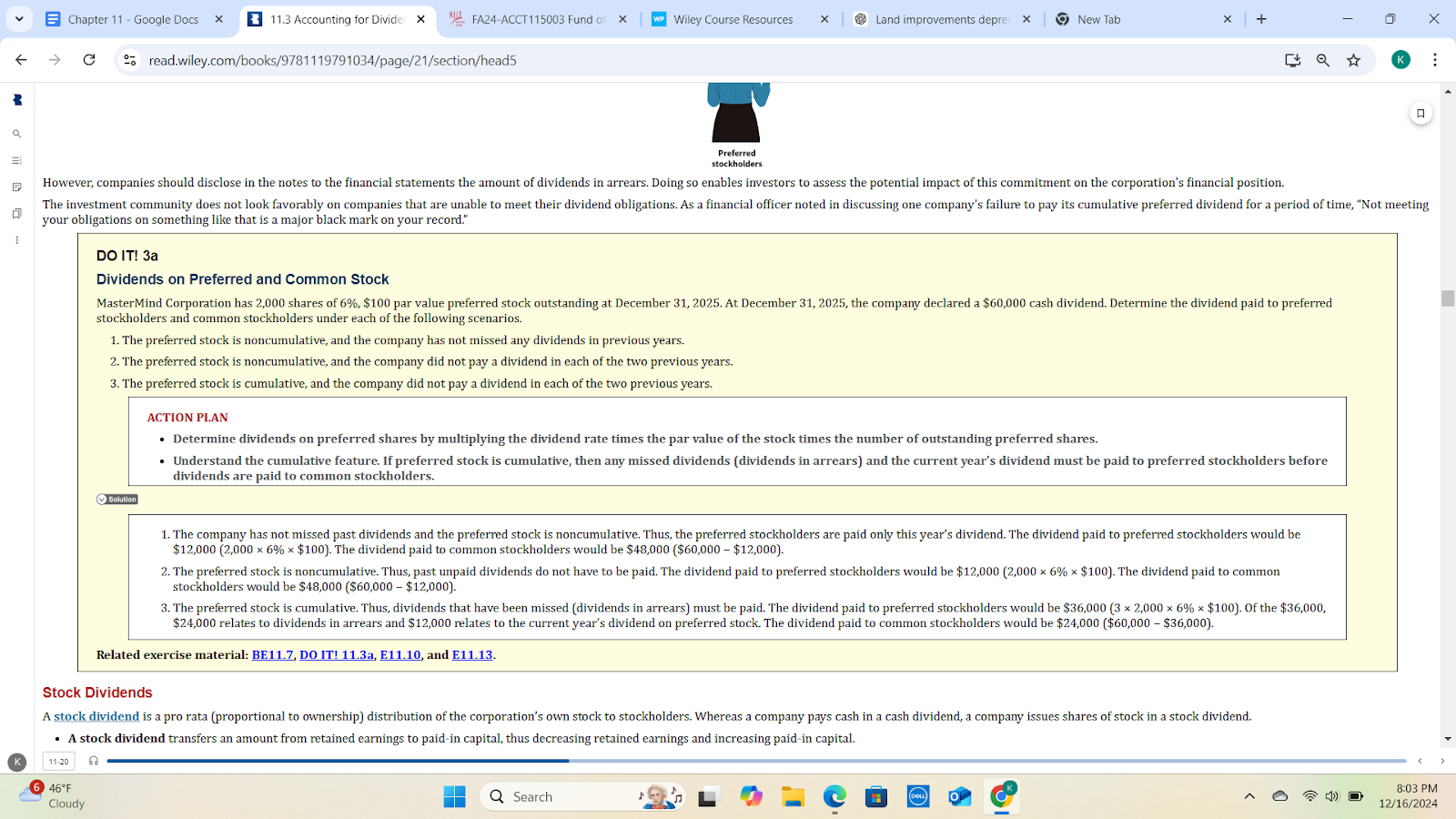

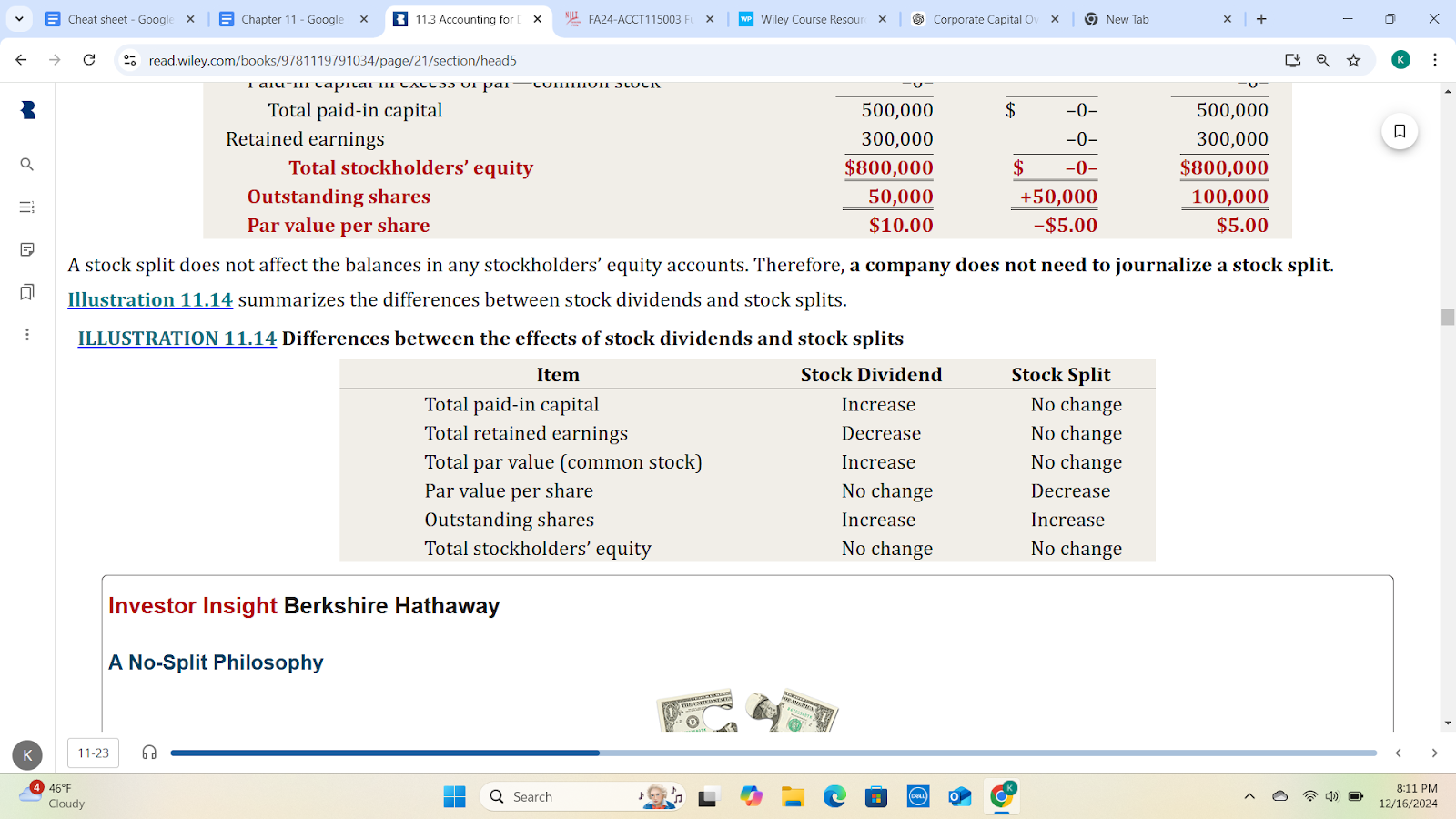

Dividends

To pay dividends, a company must have:

- Retained earnings

- Adequate cash

- Declared dividends

Declaration date: The company makes an entry to recognize the debit in Cash Dividends and the increase in the liability Dividends Payable.

Record date: No entry is required.

Payment date: Payment of the dividend reduces both current assets and current liabilities. Debit dividends payable and credit cash.

Key Financial Ratios

Payout ratio measures the percentage of earnings a company distributes in the form of cash dividends to common stockholders. It helps users determine the portion of a company’s earnings paid out in dividends.

Earnings performance (return on common stockholders’ equity) measures profitability. It helps users determine a company’s return on its common stockholders’ investment.

Higher profit (higher ROA) generally leads to higher returns for stockholders.

More debt can lead to higher potential returns (if used wisely), but also higher risk.

Cash Flow Analysis

Although depreciation expense reduces net income, it does not reduce cash. The company must add it back to net income to negate the effect of the expense and arrive at net cash provided by operating activities.

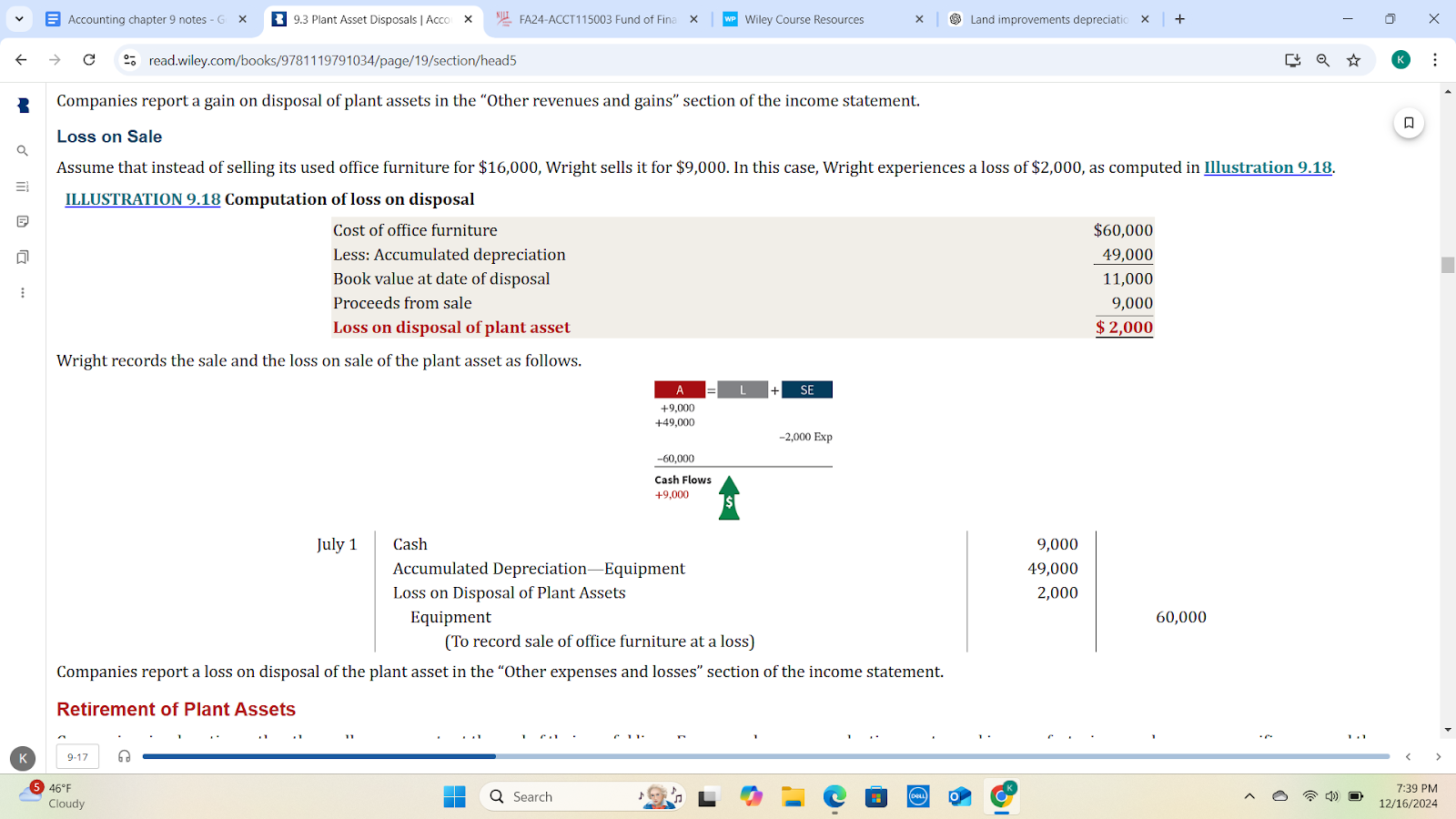

Loss on Disposal of Plant Assets

Companies eliminate all gains and losses related to the disposal of plant assets from net income to arrive at net cash provided by operating activities. A loss on disposal reduces net income but is a non-cash item.

To arrive at net cash provided by operating activities, the company must add the loss back to net income in the indirect method, as the loss didn’t affect the company’s cash.

If a gain on disposal occurs, the company deducts the gain from net income to determine net cash provided by operating activities.

Changes to Non-Cash Current Asset Accounts

Deduct from net income increases in current asset accounts (Accounts Receivable, Inventory, and Prepaid Expenses), and add to net income decreases in current asset accounts, to arrive at net cash provided by operating activities.

- If accounts receivable increases, deduct from net income (and vice versa).

- If inventory decreases, add to net income (and vice versa).

- If prepaid expenses increase, deduct from net income (and vice versa).

Changes in Current Liabilities

Add to net income increases in current liability accounts and deduct from net income decreases in current liability accounts to arrive at net cash provided by operating activities.

- Increase in current liabilities (e.g., accounts payable, accrued expenses): Add to net income.

- Decrease in current liabilities (e.g., accounts payable, accrued expenses): Deduct from net income.

Income Tax

When Income Taxes Payable decreases, it means the company paid more taxes than the expense recorded. This results in deducting the decrease from net income when calculating net cash provided by operating activities.

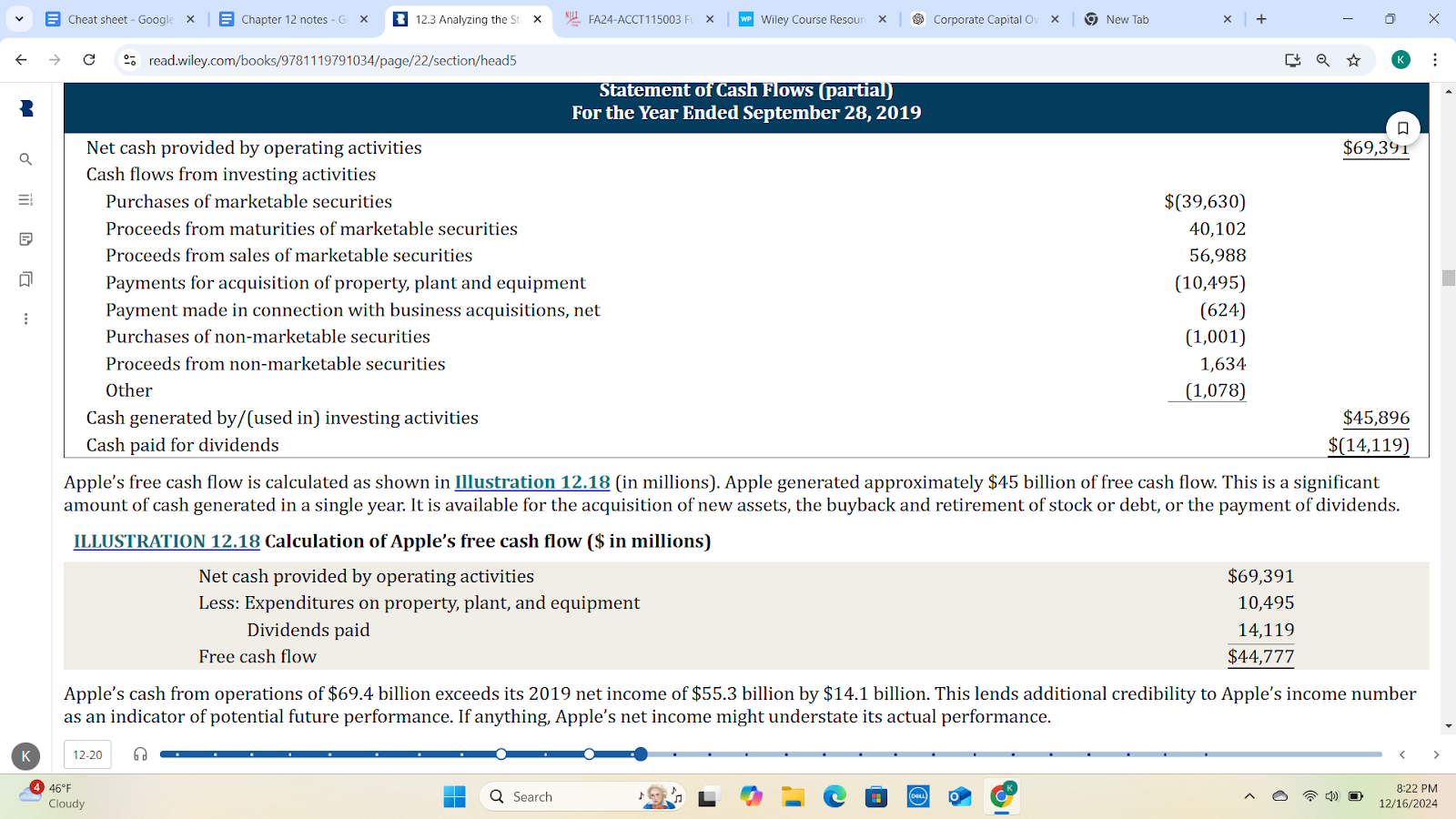

Free Cash Flow

Free cash flow helps users determine the amount of cash a company generated to expand operations or pay additional dividends.